Decatur First Bank Branches to Close, Layoffs Total Six to Date

Decatur Metro | November 8, 2011

An update on takeover of Decatur First Bank by Fidelity Bank.

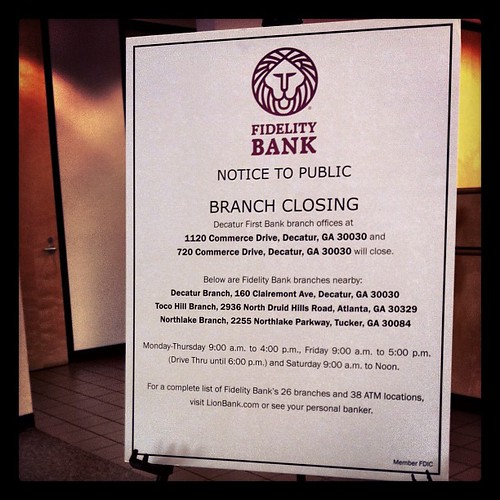

Carl Black took this picture of the sign at what was once the main branch of DBF yesterday, which announces that both the main Commerce Drive office and the Kroger satellite locations will close. Carl reports that Fidelity must provide 30 days notice to customers before doing so, but the plan is to close both branches before Christmas.

In related news, an inside source tells DM that six former Decatur First Bank employees have been laid-off to date due to the change in ownership.

I figured the main branch would be consolidated with Fidelity’s Decatur branch, but I was really hoping the Kroger satellite would remain – it’s so nice to have that option for multi-tasking! Any word on what bank, if any, will take that spot?

This is pure speculation but I bet Kroger would love to have that space back. It’s probably too small for a Best Bank or other supermarket bank specialist.

I’m going to go ahead and complain that Toco Hills and Tucker are hardly “nearby” at Decatur’s walking- and biking-friendly scale.

(The Clairemont Ave branch is certainly as convenient as the ex-DFB location, but no idea whether there’s bike parking at that building.)

If you’re looking to switch banks, Cornerstone is a good small one, and they have a branch right in downtown Decatur.

+1 (Full Disclosure: I work for Cornerstone)

Wow. Not exactly a surprise, but still stinks– especially for the laid-off employees. I hope they find new jobs quickly.

First they take away the popcorn, now they take away the super convenient location. Dang!

But they do have cookies!

I really don’t understand why you would acquire the assets of a bank, and go through that whole painful process, when you’re just going to piss off the depositors and force them to change banks.

What would you suggest as an alternative under the circumstances?

Cornerstone or Delta Community CU are probably my top 2 choices but I’m still looking.

But I’m certainly not going to stick with Fidelity since they have treated our friends, neighbors and collegues like crap over the past couple of weeks, closed our branches, and, of course, taken away the popcorn.

I no longer feel welcome so I will leave and I encourage all former DFB customers to do the same. Almost everyone I have talked to says they have or will.

Sorry, I think you missed my point. I wasn’t asking about alternatives in terms of another bank for customers, I was asking what you think the alternative would have been for DFB? They would have to be acquired by somebody or completely closed by regulators, as happened at least once in the area. Perhaps you would have preferred that or a takeover by a mega-bank?

All I am saying is that regardless of who took over the accounts, whether it be Fidelity or a Mega Bank, it seems like they would make an attempt to soothe over the transition and not fire everyone from DFB within 2 weeks and announce the closure of the branches. Doesn’t really make me want to stay or feel warm and fuzzy about Fidelity.

That’s all I was saying.

A guess, but maybe they don’t care about the deposits and care only about acquiring the loan portfolio. I don’t know much about the former DFB but would guess that it did not have a huge trove of highly profitable deposits (i.e., large and not subject to frequent withdrawals) as opposed to ordinary checking accounts with low balances.

Two other banks were bidding for DFB and were outbid by Fidelity. Neither of the other banks has a presence in the Decatur market and probably would have left the Decatur offices intact had either one outbid Fidelity. Quite frankly, Fidelity probably overpaid for DFB. It was an unlikely liquidation scenario as DFB had a healthy deposit base of local funds rather than brokered deposits, which is what made it so attractive to Fidelity.

I hope the DFB office on Commerce doesn’t become an unoccupied white elephant for years to come. Artisan residents and Ted’s employees will appreciate the parking (unless Fidelity does something insane like blocking it off).

The weekend of the shutdown the employees became temps working for an outside agency, not Fidelity Bank. As such there has been absolutely no severance pay of any kind for anyone who has been canned so far and there will be none for anyone else whose services are no longer needed from here on in. This is perfectly legal but morally repugnant IMHO.

I have heard from two former employees today something even more disturbing. All were informed on Sunday 10/23 that DFB had prepaid the Bank’s portion of health insurance for 90 days. Fidelity has since rescinded this. I imagine this is legal under the loss share agreement between Fidelity and the FDIC. Again, I find it morally repugnant that this extra burden has been placed largely on support staff who are probably trying to store as many chestnuts as they can before the inevitable downsizing that will result from shutting down two offices, a deposit operations department, and a loan operations department.

Had the five employees who were laid off on Monday been laid off the previous Friday, they would have been eligible for an unemployment benefit for the week of 10/31. Because they worked one day that week, however, they were not eligible for any benefit until 11/7. I bet each one of them could use that $330. I guess nobody in the Fidelity HR department considered this timing issue.

An employee I know who was let go on 10/31 has yet to receive any kind of separation notice or advice of COBRA rights.

Sometimes when things are as wrong but as legal as this, the only comfort I can get is knowing that some folks are going to be in Roman Catholic purgatory for a very long time…..

At that meeting on Sunday 10/23 a big deal was made about Fidelity’s chaplain. He strolled around and gave his card to all the DFB people. There was no sign of him on the day that the layoffs began. I wonder if Fidelity shouldn’t take a look at what happened to HomeBanc and Integrity Bank, two other local financial institutions that loudly trumpeted their Christian values. Perhaps they’ve bought enough plenary indulgences to stay out of purgatory.

Can someone explain to me what makes a bank “Christian”? I’m kind of weirded out by the thought. Thanks.

I second that notion. A bank has a chaplain? I can only hope he is as cool as Father Francis Mulcahy – the only other out of place chaplain that I can think of.

This Time article referenced Integrity Bank in Alpharetta while it was still flying high:

http://www.time.com/time/printout/0,8816,1090905,00.html

The COBRA notice would come through a third party insurance administrator and usually takes a little while.

I believe they legally have two weeks to get the Cobra notice to the laid off employee.

If there is one thing that should have been made abundantly clear the last few years, it’s that morality and the financial system are at best passing strangers.

If there is one thing that should have been made abundantly clear the last few years, it’s that morality and the financial system are at best passing strangers.

This stinks as the reason I bank at DFB are the folks.

One other question, anyone know if the no ATM fee policy (ie, no ATM service fees if you dont do a bunch of transactions) is going away?

re: ATM fees for non-Fidelity machines:

“we’ll even reimburse you for three foreign ATM usage fees, up to $10 monthly, when you provide the receipt.” The Lion-Lady claimed that they would reimburse if you phoned-in your request.” LION website.

This whole transition started nicely enough. The smiley Lion Lady greeted me at the branch, and I got a phone call from our new account rep (we have several business accts and loans). But, I agree with the sentiments above. They are presumably paying a premium for the DFB customers, so why piss off your newly-acquired assets?

In bank marketing, they like to talk about the “stickiness” that having customers wired into your online banking offers. The ultimate stickiness for DFB came from the 1) its folksy community focus 2) Kroger Branch, late & Sat. banking, 3) no ATM fees (and some may argue the popcorn).

So, the fact that Fidelity jettisoned the key brand differentiators is par for the course for the bean counters (If you haven’t guessed, I’m in marketing). So, now Fidelity has brilliantly (sarcasm) positioned itself to make Wells Fargo far more appealing to people like me where convenience trumps all (i.e. Wells Fargo’s coast-to-coast footprint, ATMs, superior electronic services, Drive-Thru across from Kroger etc.

Another plug for Cornerstone. Personal checking is completely free and foreign ATM fees are waived.

Heaping scorn on Fidelity is unjustified. Is it Fidelity’s fault that Decatur Firstbank management and BOD committed assets on risky loans in distant counties at the peak of the housing bubble? No.

Change banks if you want but don’t be so quick to crucify the local bank that FDIC invited to pick up the pieces left by those who have proven to be better at understanding popcorn than banking.

“those who have proven to be better at understanding popcorn than banking”

I don’t think that’s entirely fair, but there were certainly worse alternatives, like completely closing the bank or takeover by a mega-bank.

<>

What’s unfair about it? The popcorn was always hot and fresh and not over-salted.

Re-reading my comment does indeed sound scornful. I think I’m just really pissed about the loss of my beloved Kroger branch. I’d be curious about the ultimate ROI on offering that service to the customers.

I have no scorn for Fidelity and never had any relationship with DFB, but since Fidelity wanted DFB it makes me wonder. Also, there is no excuse for not treating people with respect. Many, if not most of the people who worked at DFB likely had little to do with the decisions that caused the problems, and now you have real people with real families who are losing their jobs at the start of the emotionally charged holiday season. How much would it cost Fidelity to just be nice? Having a chaplain and having a heart are not the same thing. Hopefully someone from Fidelity is reading this blog and knows people are paying attention.

I am still inconsolable. I just loved my baby bank, with its ‘roots in Decatur’. Everything about it was so…Decatur.

Still, Fidelity has cookies and great customer service.

I’m willing to give Fidelity a shot. They’re local enough. And sound. Hopefully, I’ll see some familiar DFB staff there. I want Fidelity to know that I really like using my ATM card anywhere up to 10 times a month, free. You can keep the cookies. But if ATM policy changes, I will look at other options.

. . . and a branch right across the street from the DFB main branch that’s being closed.

I feel the same, Cheyenne

I was a Decatur 1st customer, but I will not be a Lion Bank customer. Their HR policies are not accidental. I loved everyone at Decatur 1st and out of loyalty to them and being FED UP with banks I moved my account to Emory Credit last weekend.

I don’t get the logic of changing banks because of Fidelity HR policy. If former DFB depositors move their assets to another bank or credit union, what do you think Fidelity will be forced to do with former DFB staff?

The old DFB building is in a prime location. I can’t see it being empty for too long. I wonder what will go there?

Delta Community Credit Union?

Or another Credit Union?

That would kind of like McDonald’s selling to Burger King. Probably won’t happen.

Trader Joe’s of course

As I said before, the building itself may well be owned by the holding company, which was not acquired and still exists. Unless there is something in Fidelity’s agreement to the contrary, the holding company could sell or lease it to anyone they want.

Children’s shoe store, bagel place, large retail European style bakery ( I like Cakes and Ale but it’s more of an eat-in cafe than a take-out bakery like Alon’s.) Lather, rinse, repeat.

I’d like to see a drive-in liquor store in response to the new Sunday sales referendum